SpaceX Dominance Virtue or Flaw

SpaceX Dominance Virtue or Flaw

Does a golden future await or will SpaceX fall victim to their success

SpaceX were built to develop efficient space transport, and managed to marginalize the competition through extremely effective execution. Normally when a company achieves market dominance it can lead to poor outcomes, but SpaceX are far from normal… The company plays by different rules, so we should expect some divergent outcomes. Let’s review the current situation to gain some perspective, and see where all this is heading:-

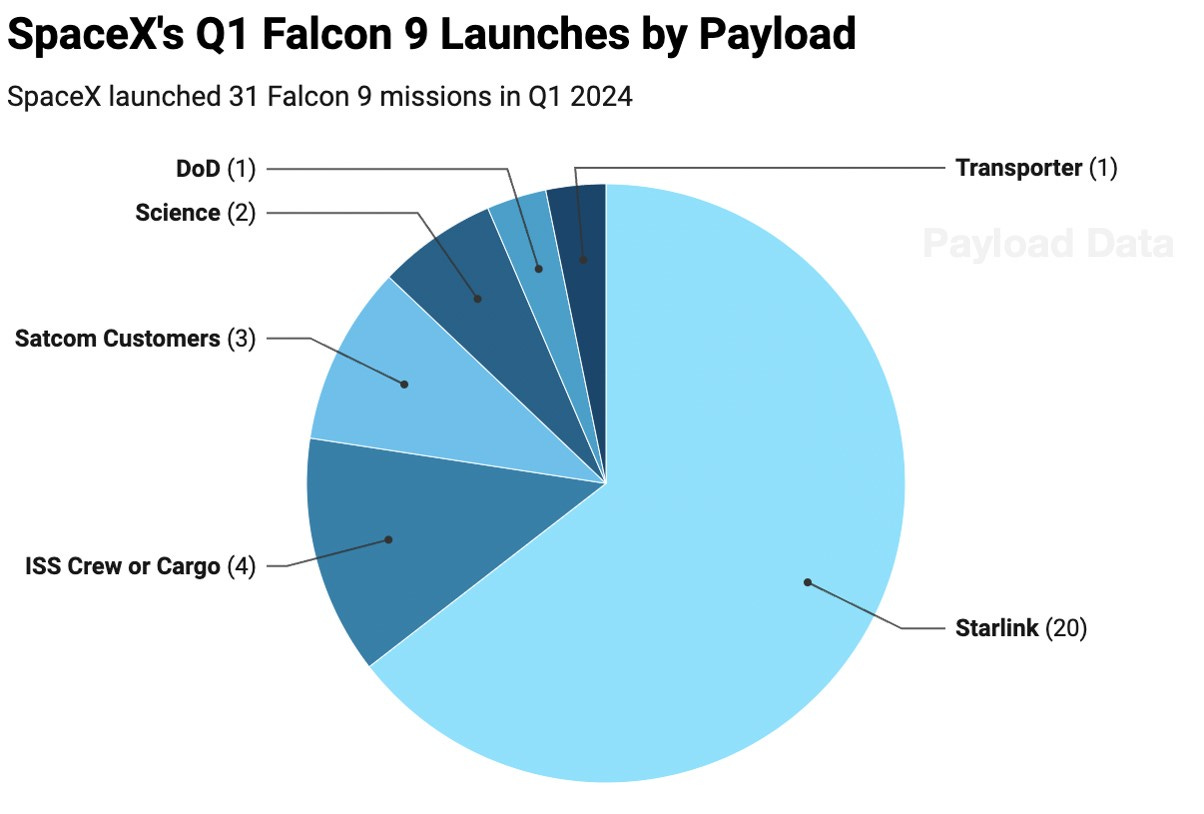

Launch dominance – in 2023 SpaceX launched ~80% of the payload sent to space, and on target to launch ~90% this year. Around two thirds of this payload figure consists of Starlink satellites which provide commercial broadband to civil, commercial and defense customers.

However, these Starlink launches give them a considerable advantage in scale – they aim to build ~200 Falcon upper stages this year alone.

“Falcon launched 67 missions in the first 6 months of 2024, delivering nearly 900 metric tons to orbit so far this year” ~ SpaceX

Launch competitiveness – SpaceX’s Falcon 9 and Falcon Heavy rockets employ reusable boosters, allowing them to recover and reuse more than 70% of the vehicle after each flight. This has proved so economic that incumbent launch companies, United Launch Alliance (ULA) and Arianespace, felt compelled to design new launch vehicles in order to compete. Unfortunately, these competitor vehicles are not reusable, which makes them overpriced for most commercial applications.

Defense sector – US military launches are normally shared between ULA and SpaceX on a 60-40 basis. However, ULA only managed one defense mission in 2024, with their Delta IV Heavy launch vehicle which has since retired. Their backlog of missions will fly on their new Vulcan Centaur vehicle, although these flights will likely slip into 2025 due to delays in development and certification. By comparison, SpaceX should perform 8 missions for the US Department of Defense in 2024 plus 4 more for non-US defense customers. ULA is joint owned by Boeing and Lockheed, although they are trying to sell the company, with little success so far.

Crew launch – SpaceX and Boeing have both developed crew vehicles to shuttle astronauts to the International Space Station (ISS) for NASA. SpaceX’s Crew Dragon performed its first operational flight in 2020, while Boeing’s Starliner encountered a series of technical setbacks which could delay it for years. This suggests Starliner will have little time to operate before preparations begin to deorbit the station, starting in 2029 (using a SpaceX deorbit vehicle).

“SpaceX has completed all six of its original crew flights for NASA, while Boeing is at least a year away from starting operational service with Starliner. In light of Boeing's delays, NASA extended SpaceX's commercial crew contract to cover eight additional round-trip flights to the space station through the end of the 2020s.” ~ Ars Technica

In fact Crew Dragon has proved so competitive and convenient, it has also been used to perform 4 commercial astronaut missions so far, with another 5 booked for the future.

Spacesuits – NASA contracted two competing companies, Collins Aerospace and Axiom Space, to develop new spacesuits. SpaceX declined to bid for this development contract and instead built their own spacesuit using a more advanced design, better suited to their future needs and purposes. Recently Collins dropped out of this competition, leaving Axiom and SpaceX to vie for a moon landing contract. Of course SpaceX will build the Human Landing System (HLS) used for NASA moon landings, which gives them the inside track.

Lunar prospects – in the early 1970s, NASA’s Apollo moon program was viewed as too expensive, and canceled by congress. NASA’s Artemis program aims to return us to the moon, using the Space Launch System built by Boeing, which costs ~$4.1bn to launch. If history repeats, congress could eventually balk at the cost of operating SLS, which might lead NASA to seek cheaper alternatives. Alternately, NASA might want to increase the flight rate, as SLS can only launch once every two years. SpaceX’s Starship could fly every 24 hours due to full and rapid reusability, and cost as little as $50m for lunar flights, so it could accelerate the Artemis program beyond recognition. One way or another, NASA will likely transition from SLS to Starship, to ensure Artemis doesn’t run out of steam or suffer the same fate as Apollo. This would make SpaceX a mainstay of the space effort, considering they will also build and operate the lunar lander i.e. Starship HLS.

Space development – NASA want to receive a reliable service at a commercial price from contractors, which are the two main strengths of SpaceX. Legacy contractors are unable to match SpaceX’s technical ability or cost efficiency, hence try to avoid any direct competition. The bidding process to develop an ISS deorbit vehicle provides a stark example. Northrop Grumman requested a cost plus profit contract, with no limit on cost or guarantee of quality as the bid contained several technical flaws. SpaceX offered to modify their proven Cargo Dragon vehicle for a fixed price, at comparatively low cost, winning the contract with ease.

“But SpaceX did not just win on price. Its "mission suitability" score, effectively its technical ability to design, develop, and fly a vehicle capable of deorbiting the space station, was 822, compared to Northrop's score of 589. SpaceX's approach had one weakness, compared to seven weaknesses in Northrop's bid, according to NASA evaluators.” ~ Ars Technica

Overall this implies SpaceX have a lock on civil, commercial and defense sectors, because other companies seem unwilling or unable to compete. Significantly, SpaceX’s dominance will likely increase over time, due to their extraordinary dedication and unrivaled technology.

Succinctly: success breeds success.

The Way Ahead

Keep reading with a 7-day free trial

Subscribe to Chris’s Substack to keep reading this post and get 7 days of free access to the full post archives.